Every year the IMF examines the Dutch Caribbean's foreign reserves and, for the most part, calls them adequate. The easy story writes itself: the islands are covered.

That story is wrong.

Reserves are built to defend the currency peg, not to pay for a disaster. When a shock arrives and nothing else has been arranged, the reserves get spent anyway, as a fund of last resort that nobody planned. It is the most expensive way there is to carry the risk, and the interesting story sits one layer down.

What the data actually says

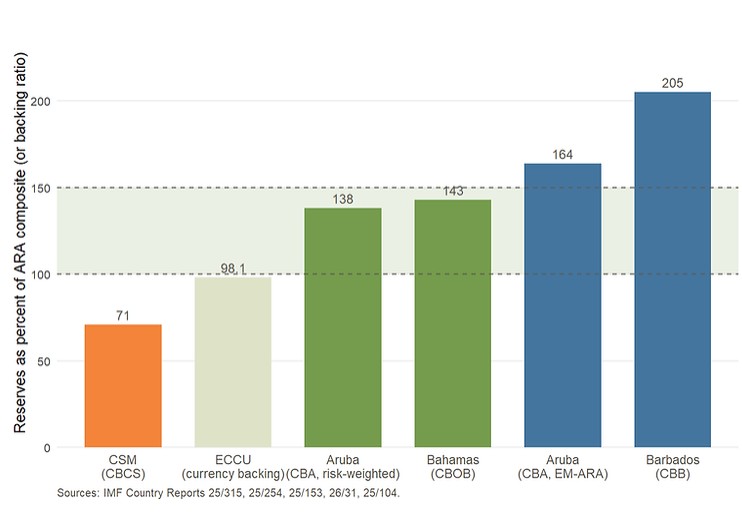

Line up five Caribbean central banks and the reserves fall about where you would expect. Barbados sits high, at 205 percent of the IMF's adequacy metric. Aruba and the Bahamas sit inside or just above the adequate range. Curaçao and Sint Maarten sit below it, the tightest position in the group.

Reserve adequacy across five Caribbean jurisdictions, end-2024. Bars show reserves as a percent of the IMF's adequacy metric; the shaded band marks the 100 to 150 percent adequate range. Curaçao and Sint Maarten sit below it. Source: IMF Article IV staff reports, 2025 and 2026.

The number that matters is not on the chart. It is what these countries do with the disaster risk the reserves are quietly absorbing. The Eastern Caribbean, Barbados and the Bahamas have spent the past fifteen years building out a set of instruments that carry that risk far more cheaply than reserves ever could. Aruba, Curaçao and Sint Maarten have bought almost none of them. A calculation for a comparable Caribbean economy puts the cost of the do-nothing default, cutting the budget to pay for reconstruction after the fact, at roughly three times the cost of arranging insurance in advance.

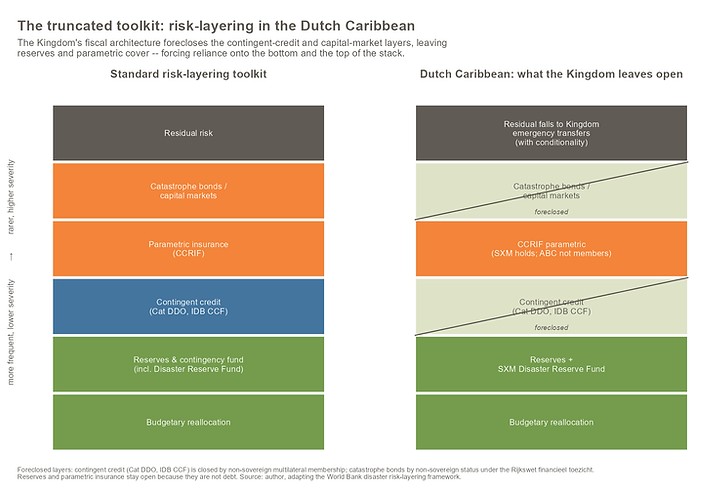

The truncated toolkit

Disaster finance comes in layers, each priced to a different slice of the risk. At the cheap, frequent end sit budget reserves. Above them sits parametric insurance, which pays out automatically within about two weeks when a measured hazard crosses an agreed threshold, with no drawn-out damage assessment. Above that sit pre-agreed emergency loans a government can draw the moment a disaster is declared. At the very top sit catastrophe bonds, sold to investors. The efficient strategy is to match each slice of risk to the cheapest instrument that can bear it, and to hold expensive reserves only for the small, frequent shocks at the bottom.

The standard risk-layering stack (left) against the version the Dutch Caribbean can actually assemble (right). The greyed layers are foreclosed by the Kingdom's financial-supervision architecture; reserves and parametric insurance stay open because they create no debt. Source: Cornerstone Economics WP-2026-02.

The Dutch Caribbean can assemble only the bottom of that stack. The reason splits cleanly in two, and telling the two halves apart is the whole point.

What is closed is not the islands' fault

Some of the toolkit is genuinely shut to them, and shut for a structural reason. As autonomous countries within the Kingdom rather than independent states, Aruba, Curaçao and Sint Maarten are not borrowing members of the World Bank or the Inter-American Development Bank. The pre-agreed emergency credit lines and the catastrophe bonds their independent neighbours use run through a membership the islands do not hold. No amount of good management on the island opens that door. It is a feature of the constitutional order.

That closed layer is not an abstraction for Aruba. Its worst exposure is not a storm but a sudden collapse in tourism, the kind COVID produced in a matter of weeks, and no insurance policy pays out on absent visitors. The one instrument designed for exactly that case, a pre-agreed line of credit a government draws when revenue falls, is precisely the layer Aruba cannot reach.

As this piece goes out, the central bank governors of the Vulnerable Twenty are in Barbados standing up a Lifeline Fund, a shared facility that pools liquidity for climate-vulnerable economies and releases it fast when a shock hits. It is close to the instrument the Dutch Caribbean needs, and it is being assembled a short flight away this week. Sovereignty is the gate, and Aruba, Curaçao and Sint Maarten are on the wrong side of it, so their names are left off the founding list.

What is open is a choice

The rest of the toolkit is open, and barely touched. Parametric insurance creates no debt, so it clears every borrowing rule the Kingdom imposes. A self-financed reserve fund is not borrowing at all. Sint Maarten holds a parametric policy and is building a disaster fund. Aruba and Curaçao hold neither.

The paper puts that gap down to which technical conversations these institutions have been part of. The central banks that took up the instruments were already inside the networks that built them, cycling staff through the facilities and the multilateral banks. The Dutch Caribbean sat at the edge of those networks, and the Kingdom relationship never pulled it in. Where the toolkit is reachable and unused, the binding constraint is not law. It is which rooms you were in.

What happened when the shock actually came

The Dutch Caribbean already ran this experiment, in 2020. Tourism stopped in a matter of weeks. Reserve drawdowns alone could not bridge the hole, no contingent financing had been arranged, and the only source of liquidity at scale was the Netherlands. The support came, at rates far below what the islands could have raised on the market, on the terms of country packages negotiated at the worst possible moment and later converted into debt. The peg held. It held because a benefactor wrote a cheque under stress, which is exactly the arrangement a pre-arranged instrument exists to retire.

There is an older idea underneath this. Independent central banks were invented to solve a commitment problem: tie your own hands in advance so you are not at the mercy of the moment when the pressure is on. Pre-arranged disaster finance does the same thing for the treasury. It fixes the terms in calm, before anyone knows whose budget the shock will land on, so the response is not improvised in the one week it can least afford improvisation.

This is larger than disaster insurance

The logic does not stop at insurance. Wherever a small state's protection depends on someone else's discretion at the moment of need, the same question applies, whether the domain is liquidity, food, fuel or medicine. Joanna Kazana, the UN Resident Coordinator, recently argued that the Dutch Caribbean is wealthy on paper and vulnerable in reality. Disaster finance is one measurable shape of that gap. A country can look solvent on every headline number and still have arranged nothing for the day the number stops describing it.

Resilience is adaptive capacity a country owns, not eligibility for someone else's transfer. Building the instruments the islands can hold in their own name is a step toward the first kind. It is worth being honest that a cheaper way to carry the current risk is still a way to keep carrying the current model, and the deeper question of whether that model should hold does not go away. But paying three times over for protection you could arrange for less is an expensive habit, and calling it resilience does not make it one.

Why Dutch readers should be paying attention

The instinct in The Hague is to read pre-arranged cover as one more claim on the Dutch budget. That gets the direction of the question wrong. Every crisis that arrives with nothing arranged becomes a negotiation in which the Netherlands writes the cheque and attaches the conditions after the fact. That role is expensive, open-ended and politically thankless, and it recurs with every shock.

A capped, pre-agreed line changes the shape of the problem for the Netherlands as much as for the islands. It bounds the Dutch exposure in advance, since the ceiling is known before any disaster is declared, and it settles the terms in calm rather than in the middle of a crisis. The reform leverage that conditionality carries does not vanish; it moves from a crisis ultimatum to a scheduled set of commitments negotiated when no one has a gun to their head. Benefactors who pre-commit reduce the moral hazard on the recipient side and the political cost on their own. The Dutch Caribbean is one of the last cases in the Kingdom's orbit where that move has not been made.

The reserves on the IMF's chart are not a disaster fund, even though they get spent as one. The next drought, fire, tourism collapse or hurricane will be paid for either way. The only open question is whether the bill was arranged beforehand, in an instrument the island holds in its own name, or scrambled for afterward on someone else's terms. Adequacy was never the right question for that. Placement is.

Click here for the report

Click here for citable archive

Author: Rendell de Kort

De Kort is an Aruban economist, principal of Cornerstone Economics and a PhD researcher at the University of Aruba and VU Amsterdam, and the author of The Conch Paradox.